There was still demand for funding using high yield-style covenants and the markets shifted, in part, towards US Term Loan B, which grew substantially over the last year—particularly in Europe.

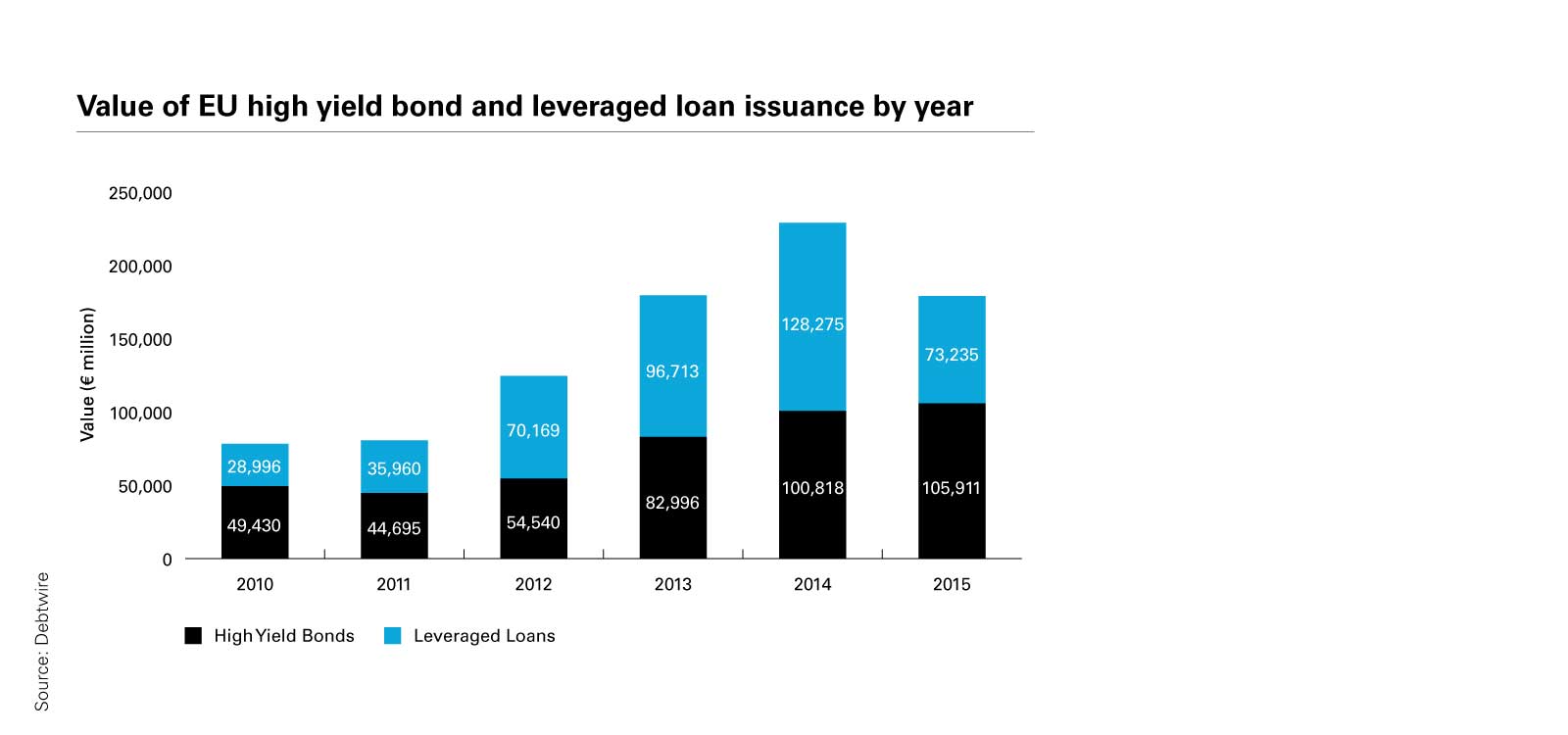

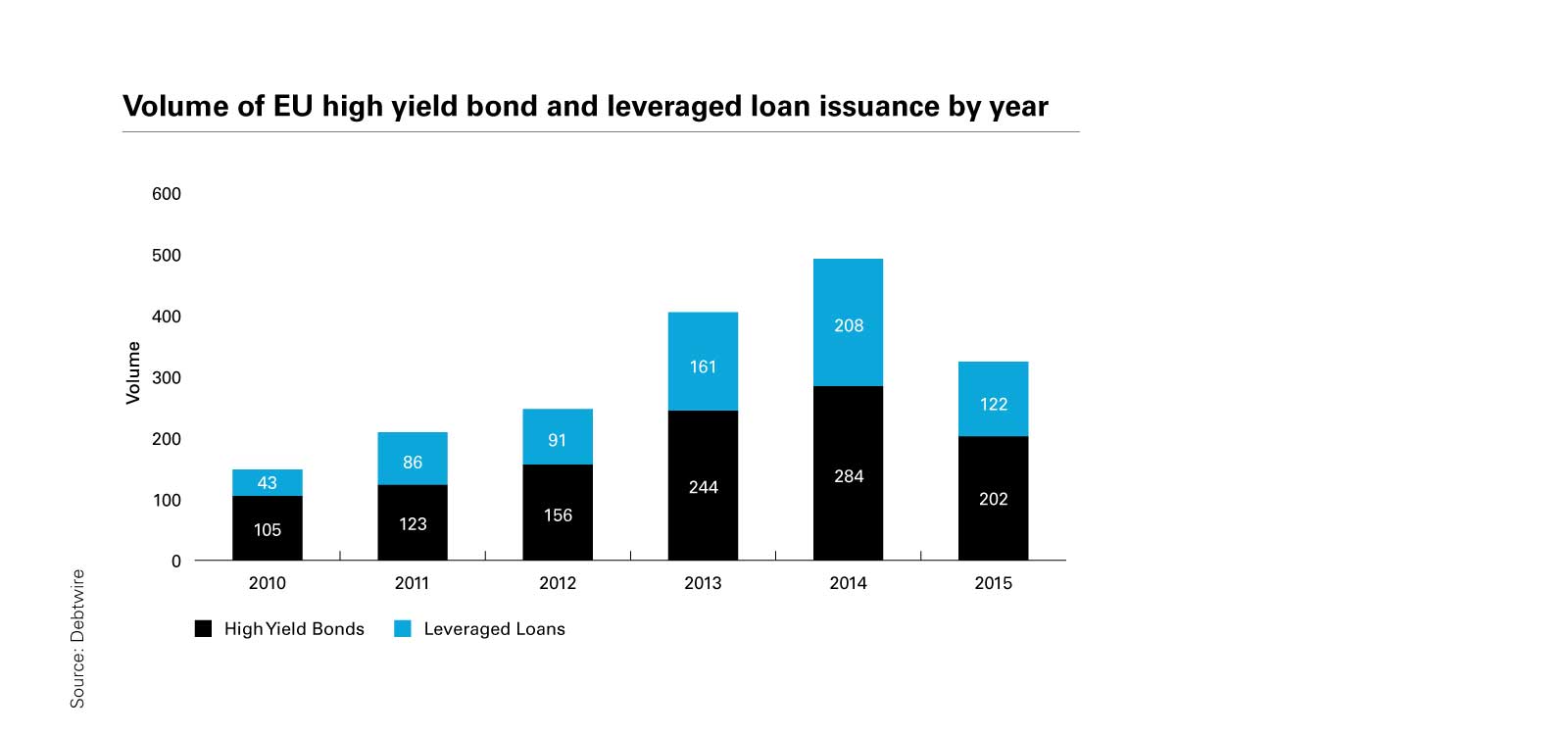

If 2014 got pulses racing in the high yield debt and leveraged loan markets, 2015 came as something of a reality check. In the first nine months of 2014, combined issuance in these two debt instruments had already surpassed the entire previous year's total by 12 percent. This €201 billion of European high yield debt and leveraged loans pushed on to a final count of almost €230 billion by the end of 2014.

Fast-forward to the end of 2015 and the story was somewhat different. Just €179 billion in high yield debt and leveraged loans had been issued by the year end, with roughly half of that total transacted in the first quarter.

Nevertheless, a strong Q4 2015 relative to Q4 2014 saw the full year value for high yield issuances surpass that of 2014, but by a mere five percent. This compares with previous year-on-year increases of 21 percent in 2014, 52 percent in 2013 and 22 percent in 2012.

Leveraged loan issuances fell by 43 percent year on year in 2015, to €73 billion.

Slowdown in the global debt markets

Geopolitical unrest and an uncertain economic outlook in several regions slowed down a high yield bond market that had taken full flight in the summer of 2014.

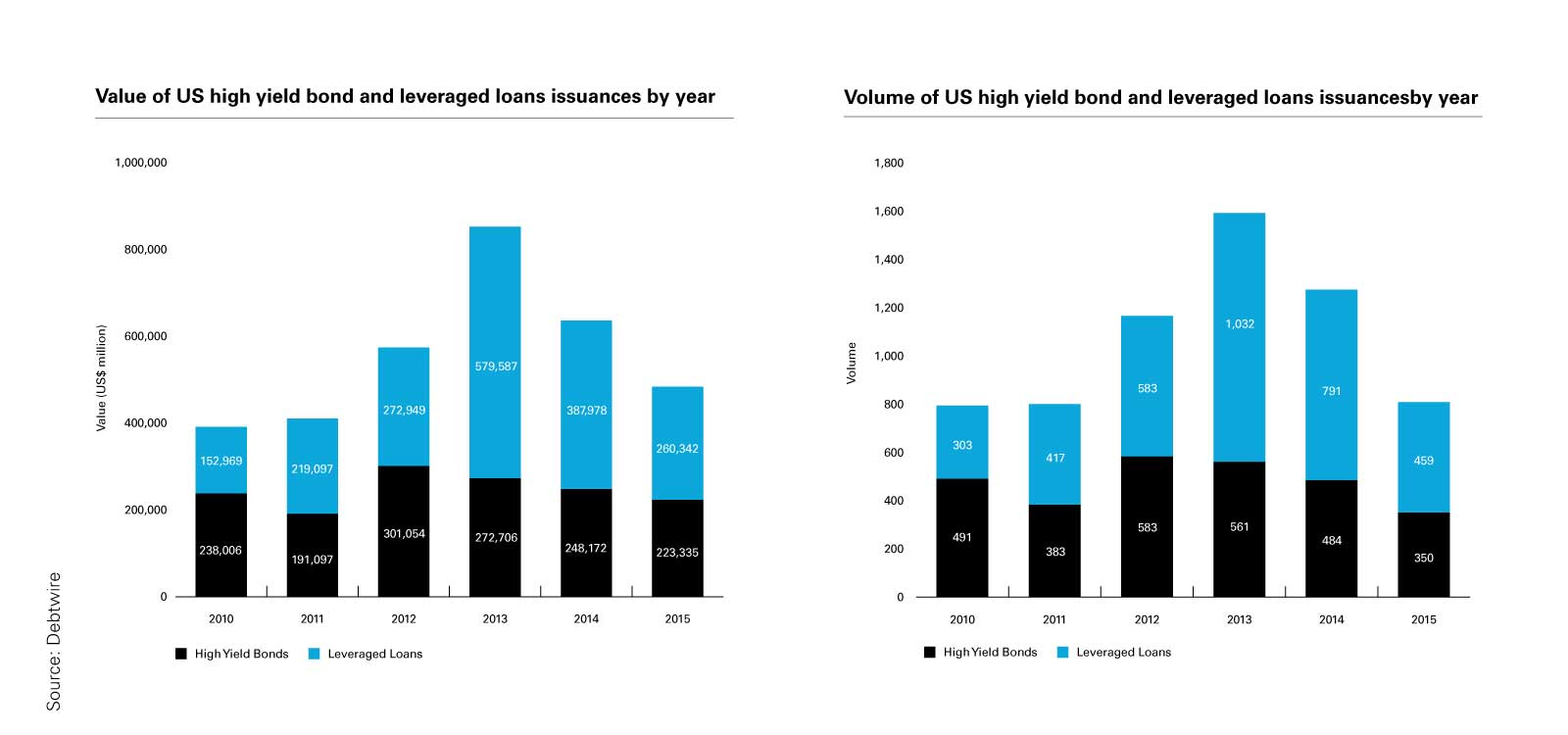

The drop in issuance was not isolated to Europe. In the far larger US market, volumes and values were down in 2015, with the second quarter responsible for the year's peak. A slump in the third quarter saw the lowest issuance of US high yield bonds in the last four years in terms of value, with barely US$223 billion being transacted in 2015 compared with US$301 billion at the market's peak in 2012. It is a similar story for leveraged loans— 2015 saw the US have its worst year of capital-raising in leveraged loans since 2011.

However, there was still demand for funding using high yield-style covenants and the markets shifted, in part, towards cov-lite Term Loan B (TLB) from instruments such as senior secured TLB. The former grew substantially over the last year—particularly in Europe.

Vast differences in economic policy have impacted debt issuance on either side of the Atlantic, but there are reasons closer to home for both of them to explain why numbers have not kept up the pace in the past 18 months. Not all of them are causes for alarm—and many will be important factors in 2016.

CASE STUDY

Cabot Financial

As international M&A heats up and complex corporate structures become the new normal, White & Case has helped create a template for sophisticated, multi-subsidiary financings.

The team advised Cabot Group in November 2015 on a transaction that amended a £200 million English law revolving credit facility agreement (including an accordion and amendments to accommodate Cabot Group's growth in certain other jurisdictions) and issued €310 million in New York law senior secured floating rate notes. The proceeds were partially used to prepay a £90 million acquisition bridge facility which was entered into in June 2015.

Additional sterling-denominated debt was also issued, taking the total existing indebtedness in the form of notes—other than the newly issued €310 million floating rate notes—to £690 million.

The deal was certainly innovative as the revolving credit facility agreement and the senior secured floating rate notes, along with the additional debt issued, are regulated by two intercreditor agreements yet secured by the same security package (with different rankings). Additionally, the security package includes, amongst other security documents governed by Luxembourg law or Irish law, two separate English law debentures, each subject to a different intercreditor agreement.

Following a major acquisition by one of its subsidiaries of the Marlin Financial Group in February 2014, Cabot did not terminate the existing Marlin intercreditor agreement regulating the debt of the acquired Marlin Financial Group due to the existence of £150 million senior secured fixed rate notes issued by a Marlin company. Instead, Cabot amended it to align with its own conditions, meaning the consolidated group's financial indebtedness has since been regulated by two intercreditor agreements.

This extremely sophisticated deal forged an innovative legal solution for acquiring companies with complex existing debt arrangements.

The rise of TLB

Cov-lite Term Loan B (TLB), in terms of covenant protection, has many similarities to high yield, though the former has typically softer call protections than those on the latter.

This debt instrument caught on in Europe in 2014 and took hold in 2015. "Cov-lite" came into fashion from across the Atlantic and the issuing community has taken note. As the rest of the bond market slowed, TLBs came into their own, with a threefold uptick in European issuance year on year.

However, despite investors' search for yield, as volatility increases investors will limit how much risk they are willing to take. The US$5.6 billion cross-border loan for tech company Veritas was pulled in November, for example, as prospective investors stayed cool on the deal due to a variety of reasons. This marked the second withdrawal of underwritten loan financing in a week, coming just after OM Group's withdrawal of a US$575 million financing round. "It's not unheard of for a bond on a best efforts basis to be withdrawn but the loan underwritten ones less so," one buy-sider told Debtwire at the time. "Market volatility is the driver behind it."

This indicates how quickly the market can change and how there can be new lines drawn in the sand for the sector as global economics shift.

While the numbers show that looser terms became very successful in 2015, issuers and their advisers have been learning, innovating and talking with investors directly to refine and understand market focus points, helping deals get to market and doing their best to ensure no one loses out if and when financial difficulty strikes.

To download the full report, please click here.

To read other articles in this report, please click here.

This publication is provided for your convenience and does not constitute legal advice. This publication is protected by copyright.

© 2016 White & Case LLP